The role of brand in M&A: Healthcare

The mergers and acquisitions (M&A) market hit record-breaking growth in 2021 and the first part of 2022, seeing the largest-ever volume of transactions and aggregate deal value globally.

Hope Schmalzried + Aaron Hall

What prompted us

From Amazon’s acquisition of MGM to Discovery’s merger with WarnerMedia, this dynamic M&A growth was not only a relative anomaly, but also an environment rich for new brand creation.

As branders with notable success in guiding such world-class companies as Bristol Myers Squibb, Glanbia and the Hewlett-Packard Company through large-scale M&As, we were interested in what this hefty transaction data could tell us about post-deal branding decisions.

More activity in the M&A market creates more opportunity for brands to come together, reposition or rebrand all together. But we wondered: did that increased activity lead to an increased number of net-new brands created over these years? Were companies leaning on co-branding approaches, or more of a pure acquisition strategy? And how, after the hundred-billion-dollar honeymoon period was over, did these companies fare?

What prompted us

What we did

We began our investigation with an S+P Capital IQ data set, which contained all public M&A transaction data in the U.S. from January 2019 to January 2023. This time frame was significant, because it encompassed both pre- and post-Covid M&A activity. We then prioritized the following industries for a deeper look:

Energy

Healthcare

Technology

Financial services

What we did

From there, we defined a set of brand metrics to evaluate for each transaction.

Did the brands:

Create a net-new, post-deal brand?

Remain independent with separate branding?

Follow an acquisition strategy where the purchased company is absorbed into the acquirer brand?

Take a co-branding or endorsed branding approach?

Wait on a branding decision pending full deal transaction?

What we expected to see

We speculated that each industry would have unique trends—and that net-new brand creation would explode during such an active period.

To these hypotheses, the data said both yes and no.

For example, branding decisions can be tracked on an industry-by-industry basis. Take the energy and technology sectors. We concluded that the former was more likely to engage in a pure acquisition strategy, whereas the latter embraced endorsed or co-branding approaches.

Yet as brand creators, we were particularly surprised by the dearth of net-new brands across industries: creation of a net-new brand occurred no more than 2% of the time across selected industries.

So, if a surplus of net-new brands was not the outcome of increased M&A activity, what were the outcomes?

What we expected to see

What we found

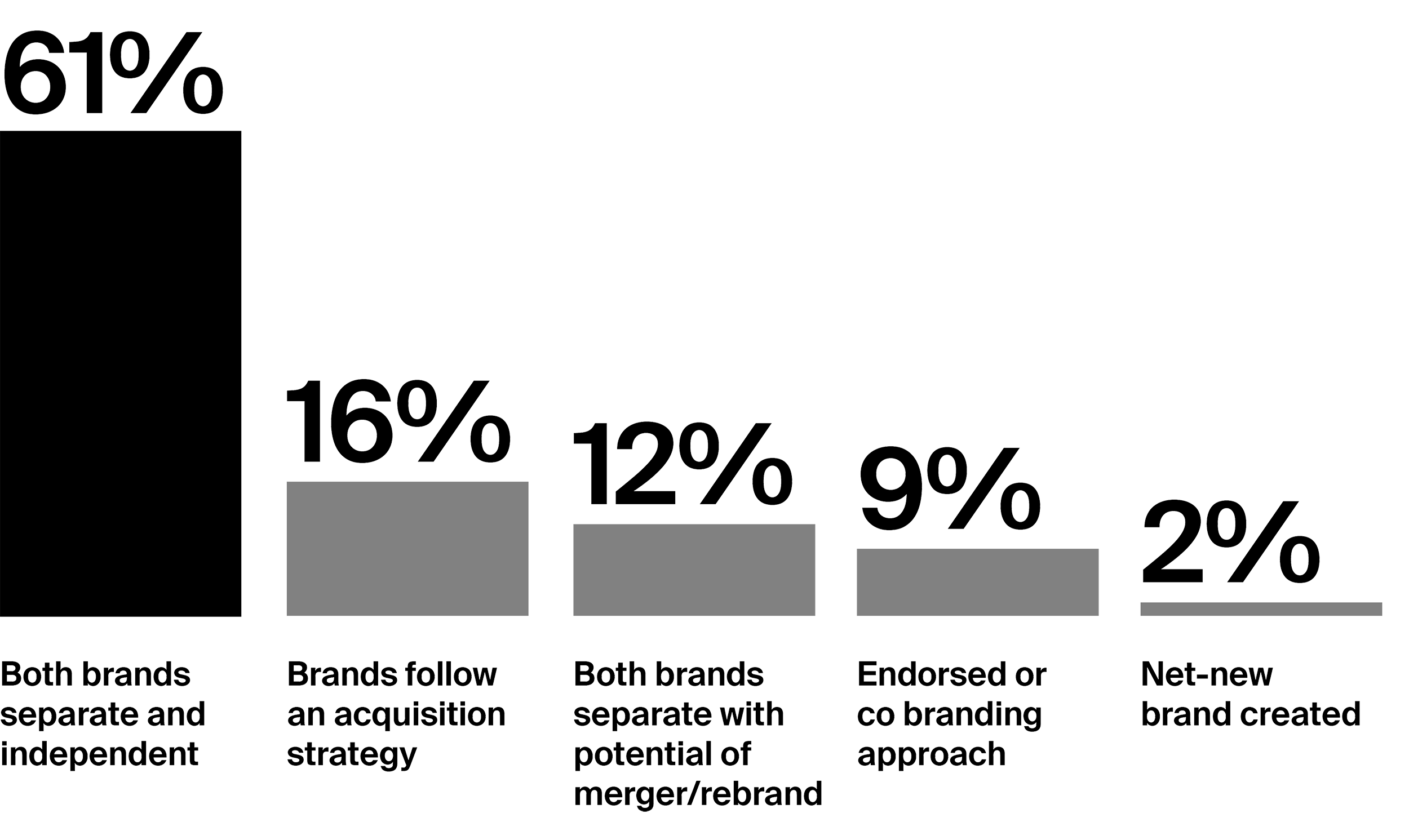

Within the healthcare sector of our data set, the most common branding decision was to keep both brands separate and independent. This occurred 61% of the time.

Retaining separate brands was the most common M&A outcome in the hospital and hospice space.

NYU Langone Health’s acquisition of Long Island Community Hospital in late 2021 is a good case study. The local healthcare provider maintained its own branding, visual design and website separate from the NYU brand. The same occurred across a number of hospice and home care agencies in the U.S. from 2019 to 2023, which were purchased by suchlarger care management agencies as Public Health Management Corporation.

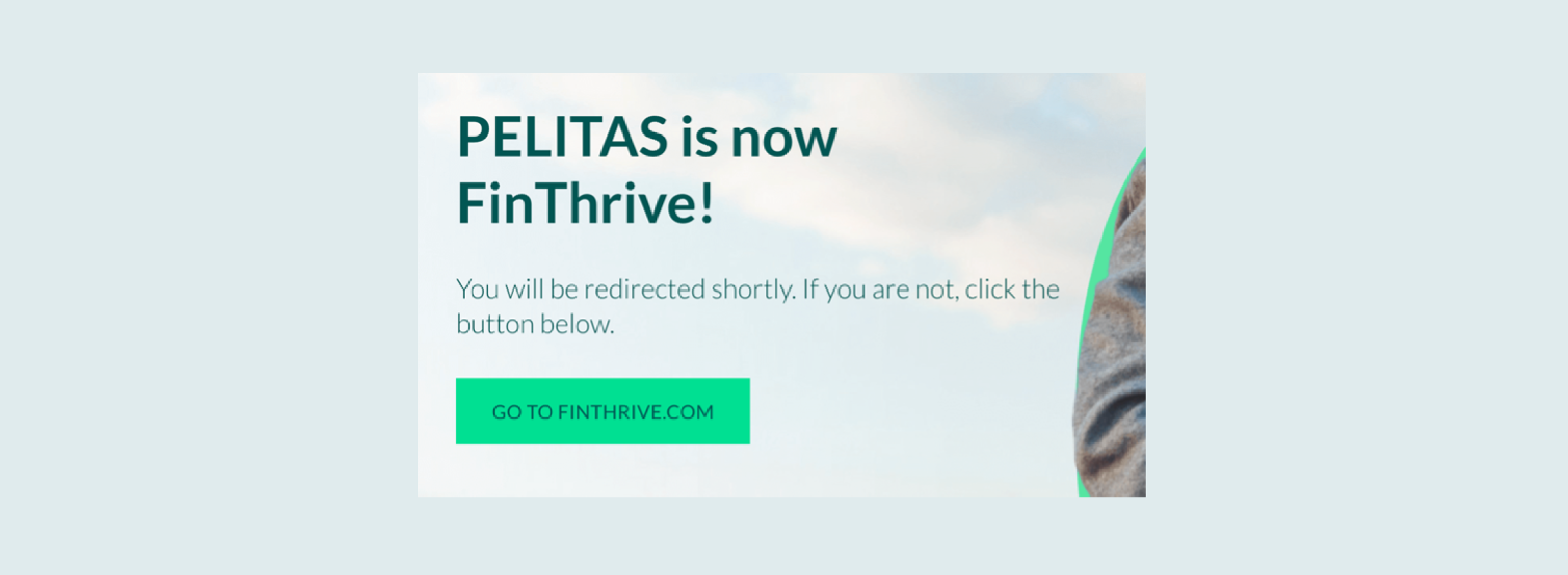

The second most popular branding decision—at 16%- was a more traditional acquisition strategy, where the smaller, purchased brand was absorbed into the larger purchasing company. This was common in health-tech or technology-adjacent companies. For instance, when nThrive (also called FinThrive) acquired Pelitas in February 2022 to round out their front-end revenue cycle management (RCM) offering for patients, Pelitas became FinThrive.

What we found

We see companies leveraging co-branding or endorsed branding efforts 9% of the time, and net-new brands being created in only 2% of the mergers and acquisitions.

New brand creation, while infrequent in nature, was also more common in the health-tech and biotech space. Roche’s purchase of Good Therapeutics typifies this trend. In September 2022, Roche created a new spin off: Bonum Therapeutics. It retains no affiliation to either the Roche or Good Therapeutics brand.

The remaining 15% of the time, M&As in the healthcare space took a “separate for now” approach, which means the brands remain independent until further notice or final deal completion. In these cases, existing language or branding choices often suggest the potential for endorsed, cobranding, or fully absorbed decisions in the future. An excellent example of this is when Amazon purchased One Medical in early 2023. While both brands currently remain independent in visual and verbal identity, the two brands have begun a more symbiotic branding and messaging approach without formally merging or cobranding, yet.

Insights

In healthcare, brand equity is paramount. Because patients trust their local hospitals and healthcare providers, these brands often have strong, existing reputations in the community. These ties are worth leveraging. This might be why brick-and-mortar healthcare has a higher percentage of mergers retaining separate brands or rolling out slow, co-branding migration strategies over multiple years. A quick migration or acquisition strategy could fail to transfer brand equity and runs the risk of losing the trust of the patients who have a relationship with the acquired brand.

Within the niche of health-tech or biotech, M&As are often solving for a gap in capabilities. Companies will buy products that integrate into an existing solution or suite of solutions—much like the Pelitas example mentioned above. In these situations, sunsetting purchased brands can be helpful in conveying a seamless and unified experience outward. Many of the benefits behind health-tech or biotechnology come from integrating point solutions together to create an optimized overall solution. Merging two brands or multiple brands is a great way to communicate this connectivity. And from a brand management and communication perspective, it can be easier to manage one singular brand as a health-tech start-up/entity continues to grow, build, and acquire.

Top of mind for many patients and consumers is the entrance of out-of-industry players into the world of healthcare. Walmart was an early mover in this space as they expanded into the optical business in the late 1990s with their vision center. Since then, several retail-first providers have partnered with pharmacies to expand their health-focused offerings. Tech-first companies like Apple have also expanded into the adjacent world of health-tech and bio tracking.

Insights

For out-of-industry players entering the healthcare space, choosing the right brand integration strategy is of utmost importance. Amazon’s purchase of One Medical is a hugely important addition to the Amazon business strategy. But Amazon has relatively little equity or reputation in the healthcare space. Amazon is clearly eager to leverage the brand equity and trust One Medical has spent years building with their patients. Amazon’s purchase of Whole Foods in 2017 might serve as another indicator for their acquisition and brand architecture strategy. While there are nods to Amazon ownership, through deal perks and exceptional delivery, the brand is not boldly present across the company’s branding and communications.

How brand can drive success

The most outwardly visible role of brand in M&A is the change—or lack thereof—made to a company’s name or logo. Think hyphens and abbreviations that run rampant and amalgamated visual identities that read more chaotic than cohesive. Because this metric of change is so easily visible, it formed the foundation for our analysis of our M&A data.

Beyond changing those important identifiers, there is other, more nuanced and powerful brand work that can be done to ensure success of a new joint entity—for leveraging brand increases the likelihood of success of the merger or acquisition.

A merger or acquisition is a perfect opportunity to revisit a company’s mission, vision and values. What’s more, with new capabilities provided by the event, it is the perfect time to refresh the brand strategy and competitive positioning.

How brand can drive success

One way to do so is to embrace brand-led organizational change.

By assessing each company’s culture and creating a careful plan for integrating the best aspects of both entities, companies can optimize cultural integration, employee engagement, operational efficiency, and productivity. Engaging employees of both companies with a clear EVP and uniting them around a new shared goal yields better financial outcomes.

While an increase in M&A activity globally and in the U.S. was notable, even more notable were the resulting branding outcomes. Where we expected to see an increase in net-new brands created, we were surprised to see no net-new brands created in the U.S. industry sector (because of M&A). Retaining separate brands was far more represented in the energy sector than other industries we reviewed. As our energy experts explained, more mature companies in the industry tend to take a more steady and patient approach to brand merging or absorption during M&A.

However, whether two companies change their names or logos or not, there is still important culture and employee brand work that companies can embark on during the M&A process to ensure cultural integration, employee engagement, and operational efficiency.

Where do you stand?

Was brand integration discussed as part of the M&A negotiations?

Do you have M&A brand guidelines?

Have you had any internal conversations about brand integration strategy?

Do you have current equity research on both of the brands?

Has your research indicated whether either brand can stretch into the other brand’s territories?

Have you considered the cost of a brand change (both brand creation and brand implementation)?

Have the cultures of both companies been reviewed/analyzed for symmetries and best practices?

Where do you stand?